The big news for the day was a U.S. federal court ruling against the legitimacy of Trump’s tariffs, causing major waves among risk assets.

While the U.S. dollar initially had a positive reaction to the news, it ultimately shed gains as trade uncertainty and additional concerns about government revenues came in play.

Here are headlines you may have missed in the last trading sessions!

Headlines:

- API crude oil inventories showed reduction of 4.236M barrels vs. estimated build of 1M barrels

- Nvidia reported stronger than expected Q1 EPS of 96c but warned that Chinese AI rivals are “formidable”

- U.S. Court of International Trade ruled that Trump exceeded his authority in imposing “Liberation Day” tariffs, which were then declared illegal and blocked via injunction

- Trump administration filed an appeal with the U.S. Court of Appeals, which temporarily reinstated some tariffs on an administrative basis, giving room for an additional delay request

- RBNZ Governor Hawkesby warned that near-term growth headwinds are coming from weaker demand and weaker inflation pressures, including uncertainty where tariffs might land

- U.S. paused exports of jet engine and chip technology to China, will begin revoking visas of Chinese students

- New Zealand ANZ Business Confidence for May 2025: 36.6 (53.0 forecast; 49.3 previous)

- Australia Building Capital Expenditure for March 31, 2025: 0.9% q/q (0.3% q/q forecast; 0.2% q/q previous)

- Australia Plant Machinery Capital Expenditure for March 31, 2025: -1.3% q/q (0.4% q/q forecast; -0.8% q/q previous)

- Australia Private Capital Expenditure for March 31, 2025: -0.1% q/q (0.5% q/q forecast; -0.2% q/q previous)

- Japan Consumer Confidence for May 2025: 32.8 (32.8 forecast; 31.2 previous)

- Another U.S. court blocked Trump’s tariffs in a case filed by two Illinois-based toy companies, Learning Resources and hand2mind, leading to a 14-day pause

- U.S. Initial Jobless Claims for May 24, 2025: 240.0k (230.0k forecast; 227.0k previous)

- U.S. GDP Price Index 2nd Est for March 31, 2025: 3.7% q/q (3.7% q/q forecast; 2.3% q/q previous)

- U.S. GDP Growth Rate 2nd Est for March 31, 2025: -0.2% q/q (-0.3% q/q forecast; 2.4% q/q previous)

- Fed head Powell met with President Trump but did not discuss monetary policy expectations and reiterated that rate changes will depend on incoming economic information

- U.S. EIA crude oil inventories down 2.795M vs. estimated build of 0.118M

- Fed official Goolsbee: Rates can go lower if tariffs are avoided by a trade deal or otherwise

- Fed official Daly warned that workers are worried about inflation

- White House announced that Israel signed a ceasefire proposal with Hamas

- U.S. Pending Home Sales for April 2025: -2.5% y/y (1.9% y/y forecast; -0.6% y/y previous); -6.3% m/m (-1.5% m/m forecast; 6.1% m/m previous)

Broad Market Price Action:

{kind=link}

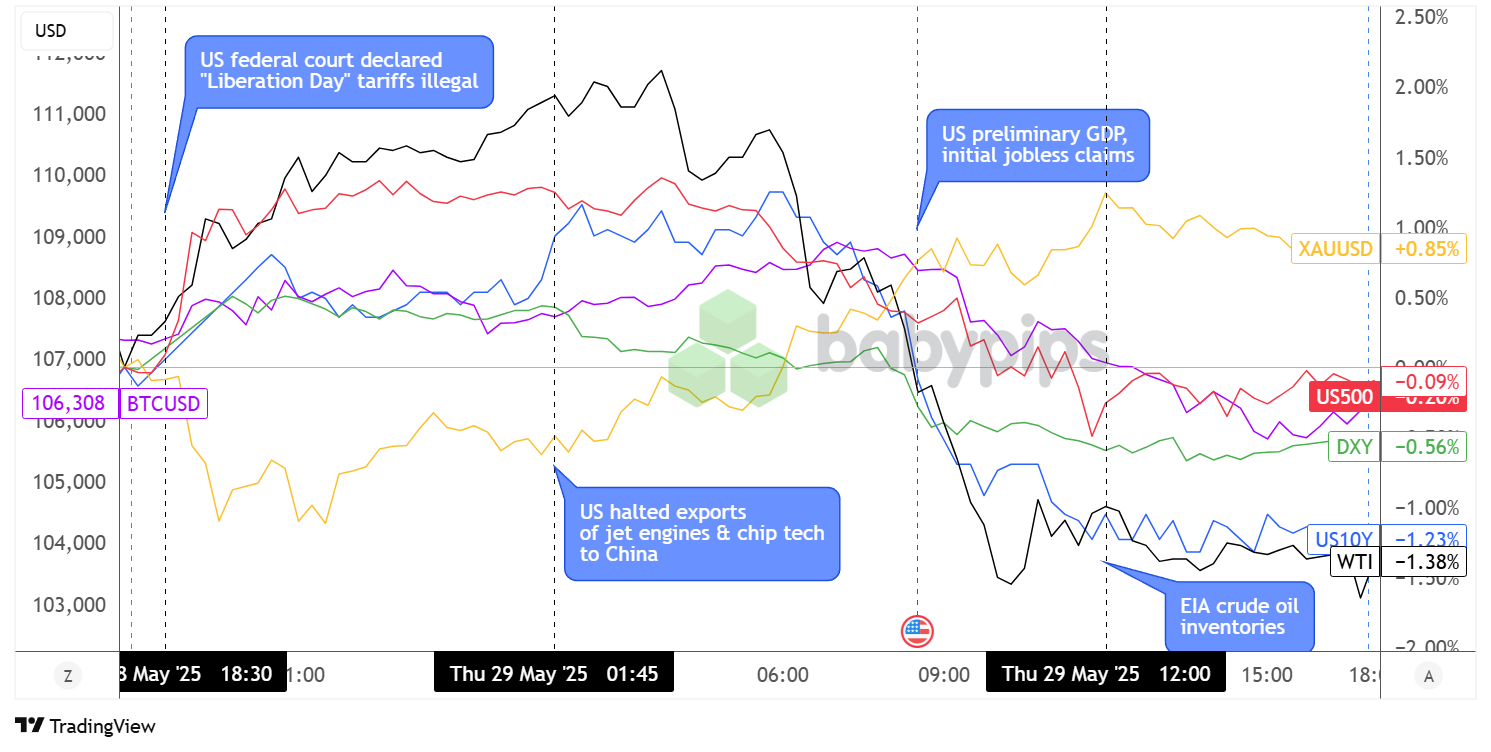

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

Risk-taking surged from the get-go, as Asian session traders were greeted by news that a U.S. federal court ruled that Trump’s “Liberation Day” tariffs were illegal because Congress didn’t exactly grant him unlimited trade powers.

WTI crude oil surged sharply, as the energy commodity also drew support from a surprise reduction in API inventories, while investors cheered the possibility of avoiding supply chain disruptions and seeing sustained global oil demand.

However, the rally peaked right around the time of the White House press conference, during which the U.S. announced it would be halting exports of jet engines and chip technology to China. The commodity bottomed out from its slide when the EIA report also reflected an unexpected draw in stockpiles but still wound up 1.38% lower for the day.

U.S. equity futures, which were also riding high after Nvidia’s stronger than expected earnings report and news of Trump’s tariffs blockage, started turning lower as trade tensions remained elevated while U.S. officials assured that the court ruling was merely a hiccup. U.S. stock indices sustained the downward momentum, although the S&P 500 managed to squeeze out a 0.40% gain while the Nasdaq caught a 0.28% increase for the day.

Treasury yields appeared to trail risk assets in rallying on a possible removal of tariffs before also turning lower when the U.S. Court of Appeals temporarily reinstated some tariffs and gave the Trump administration room to request delays. Yields also extended their drop despite some green shoots in U.S. GDP data, as the focus seemed to shift to government revenue concern amid trade uncertainty.

Gold, which appeared poised for another day of safe-haven losses early on, got its bearings back when risk aversion returned to the markets during the London and U.S. sessions. Bitcoin, on the other hand, failed to take advantage of risk-off flows as it fell through the key $107,000 barrier by the end of the New York session.

FX Market Behavior: U.S. Dollar vs. Majors:

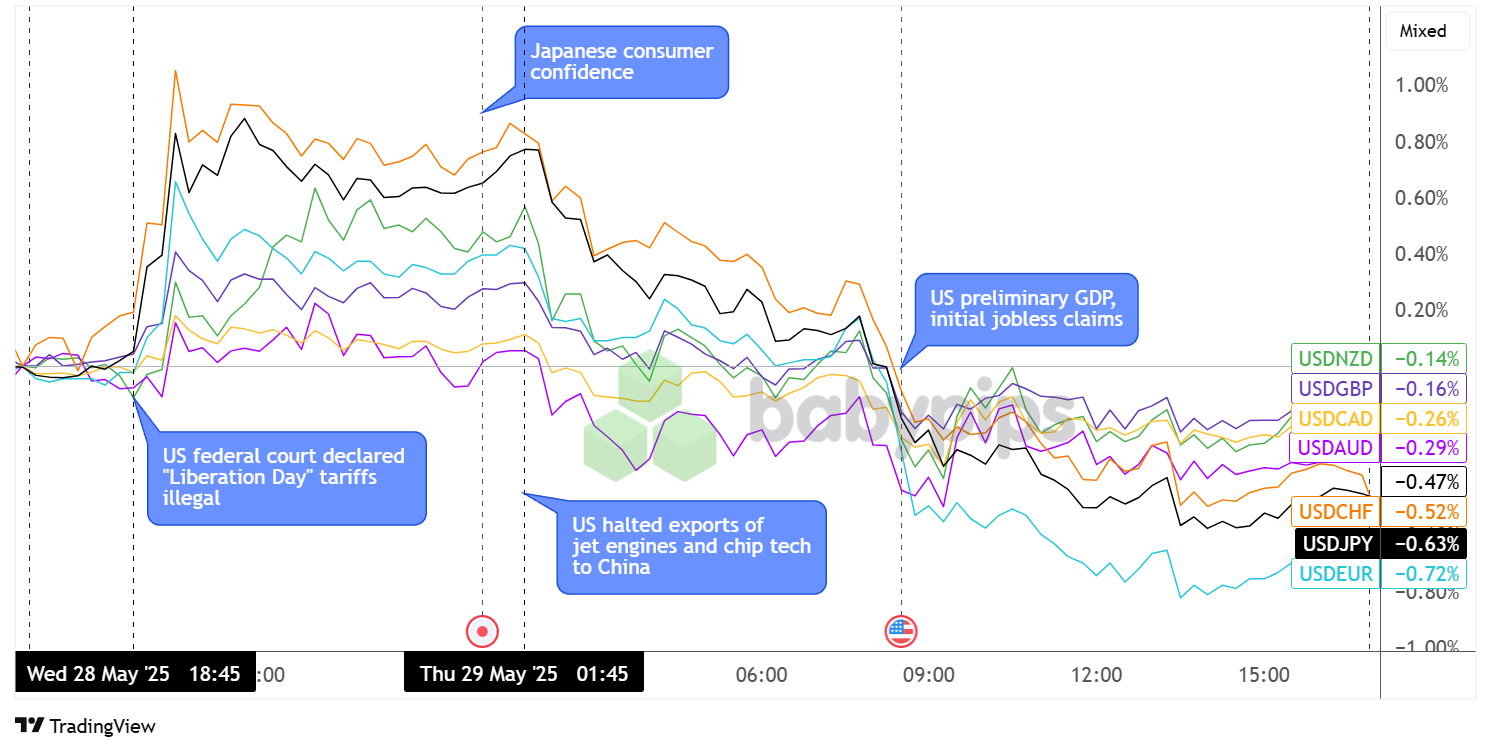

Overlay of USD vs. Major Currencies Chart by TradingView

Price action among dollar pairs was in sync throughout the day, with the U.S. currency popping higher on news that the U.S. Court of International Trade blocked Trump’s sweeping tariffs on majority of its trade partners.

However, USD gains were short-lived as the Trump administration quickly filed an appeal and eventually got majority of the tariffs reinstated on an administrative basis. During the White House press conference, officials announced that the U.S. halted exports of jet engines and chip technology to China while also saying that they will start revoking visas of Chinese students, reviving international tensions.

Investors appeared concerned about U.S. government revenue sources in case tariffs continue to be blocked, especially since Trump’s tax bill included plans to boost spending big-ly, stoking further worries about U.S. fiscal health.

The dollar carried on with its downward trajectory as U.S. data came in mixed, with the preliminary GDP seeing a slight upward revision to show a smaller 0.2% contraction in Q1 2025 and the initial jobless claims coming in higher than expected. By session’s end, USD chalked up its largest losses against EUR (-0.72%) followed by safe-haven rivals JPY (-0.67%) and CHF (-0.52%).

Upcoming Potential Catalysts on the Economic Calendar:

- Japan Housing Starts at 5:00 am GMT

- Japan Construction Orders at 5:00 am GMT

- Germany Retail Sales at 6:00 am GMT

- Swiss KOF Leading Indicators at 7:00 am GMT

- Euro area M3 Money Supply at 8:00 am GMT

- Germany CPI Growth Rate at 12:00 pm GMT

- Canada GDP Growth Rate at 12:30 pm GMT

- U.S. Personal Income & Spending at 12:30 pm GMT

- U.S. Core PCE Price Index at 12:30 pm GMT

- U.S. Wholesale Inventories at 12:30 pm GMT

- U.S. Goods Trade Balance at 12:30 pm GMT

- U.S. Chicago PMI at 1:45 pm GMT

- U.S. UoM Consumer Sentiment & Inflation Expectations Index at 2:00 pm GMT

While the market spotlight seems to be mainly on trade updates lately, top-tier inflation reports like Germany’s CPI and the U.S. core PCE price index could impact monetary policy expectations for the ECB and Fed.

After that, we’ve also got the Chicago PMI and UoM consumer sentiment index, which are considered leading indicators for growth and spending, so keep an eye out for USD volatility during these releases, too.

As always, stay nimble and don’t forget to check out our Forex Correlation Calculator when taking any trades!