Global trade developments were still front and center on Tuesday, although the market spotlight also turned to top-tier economic releases.

In particular, the U.K. jobs report and the U.S. CPI figures caused major waves among asset classes, as the former surprised to the upside while the latter fell short of estimates.

Here are headlines you may have missed in the last trading sessions!

Headlines:

- Bank of Japan Summary of Opinions (April 30-May 1 meeting) signaled an intention to hike rates further

- Trump’s economic adviser Hassett announced there are 24 more countries lined up for trade talks over the weeks

- U.S. President Trump and Saudi Crown Prince Mohammed bin Salman announced a $600 billion Saudi investment in the U.S. and a pledge for $1T in deals across many sectors

- Japanese Finance Minister Kato mentioned he wants to discuss FX with Treasury Secretary Bessent

- U.S. Trade Representative Greer warned that China tariffs can still go back up

- U.K. BRC Retail Sales Monitor for April 2025: 6.8% (1.3% forecast; 0.9% previous)

- Israeli Prime Minister Netanyahu commented that Israel’s armed forces are preparing to “finish the job” and defeat Hamas

- U.S. announced another round of Iran oil sanctions, targeting the global network shipping Iranian oil

- People’s Bank of China set CNY reference rate below 7.2 for the first time in an effort to ensure currency stability

- China lifted ban on Boeing deliveries while U.S. reduced de minimis tariffs on Chinese shipments from 120% to 54%

- Australia Westpac Consumer Confidence Index for May 2025: 92.1 (90.5 forecast; 90.1 previous)

- Australia NAB Business Confidence for April 2025: -1.0 (-5.0 forecast; -3.0 previous)

- Australia Building Permits Final for March 2025: -8.8% m/m (-8.8% m/m forecast; -0.3% m/m previous)

-

U.K. Claimant Count Change for April 2025: 5.2k (22.0k forecast; 18.7k previous)

- Unemployment Rate for March 2025: 4.5% (4.4% forecast; 4.4% previous)

- U.K. Average Earnings excl. Bonus (3Mo/Yr) for March 2025: 5.6% (5.7% forecast; 5.9% previous)

- U.K. Employment Change for March 2025: 112.0k (80.0k forecast; 206.0k previous)

- BOE Chief Economist Huw Pill said that interest rates might need to stay high since inflation could prove stronger than expected

- Germany ZEW Economic Sentiment Index for May 2025: 25.2 (12.5 forecast; -14.0 previous)

- Euro area ZEW Economic Sentiment Index for May 2025: 11.6 (-6.0 forecast; -18.5 previous)

- U.S. NFIB Business Optimism Index for April 2025: 95.8 (93.5 forecast; 97.4 previous)

- U.S. Consumer Price Index Growth Rate for April 2025: 2.3% y/y (2.5% y/y forecast; 2.4% y/y previous); 0.2% m/m (0.3% m/m forecast; -0.1% m/m previous)

- U.S. Core Consumer Price Index Growth Rate for April 2025: 2.8% y/y (2.8% y/y forecast; 2.8% y/y previous); 0.2% m/m (0.2% m/m forecast; 0.1% m/m previous)

- Germany Current Account for March 2025: €34.1B (€21.5B forecast; €20.0B previous)

- U.S. President Trump urged Fed head Powell again to cut rates

Broad Market Price Action:

{kind=link}

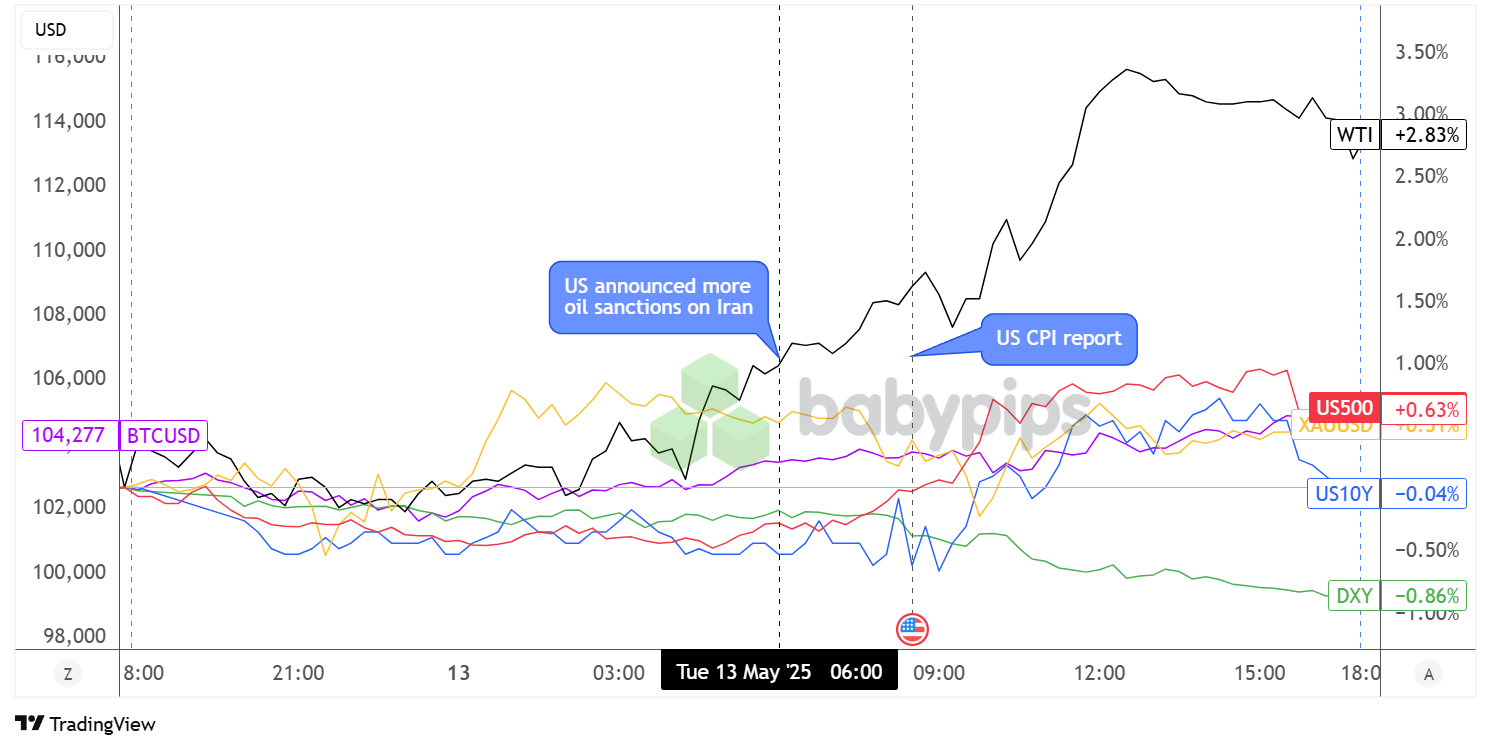

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

Markets calmed down during Tuesday’s Asian market hours after the previous trading session’s risk rallies, as traders appeared to turn their attention to what’s next in U.S. trade talks, spurring some safe-haven gains for gold.

While Trump’s National Economic Adviser Kevin Hassett shared that 24 more countries are lining up for tariffs deals, Trade Representative Jamieson Greer warned that China’s trade levies could still go up if things don’t work out. Still, China followed through by lifting its ban on Boeing deliveries while the U.S. also lowered de minimis tariffs on Chinese shipments from 120% to 54%.

WTI crude oil also drew support from another round of U.S. oil sanctions, this time targeting the global network shipping Iranian oil, reviving supply concerns while Middle East tensions remain elevated. The energy commodity extended its rally after the U.S. CPI came in weaker than expected, effectively weighing on USD while Fed easing expectations picked up.

U.S. equity indices also rallied following the CPI release while U.S. President Trump declared that “the market will go higher” and called on Fed Chairperson Powell again to cut interest rates. The S&P 500 index closed 0.8% in the green while bitcoin reclaimed the $104K handle on risk-taking.

FX Market Behavior: U.S. Dollar vs. Majors:

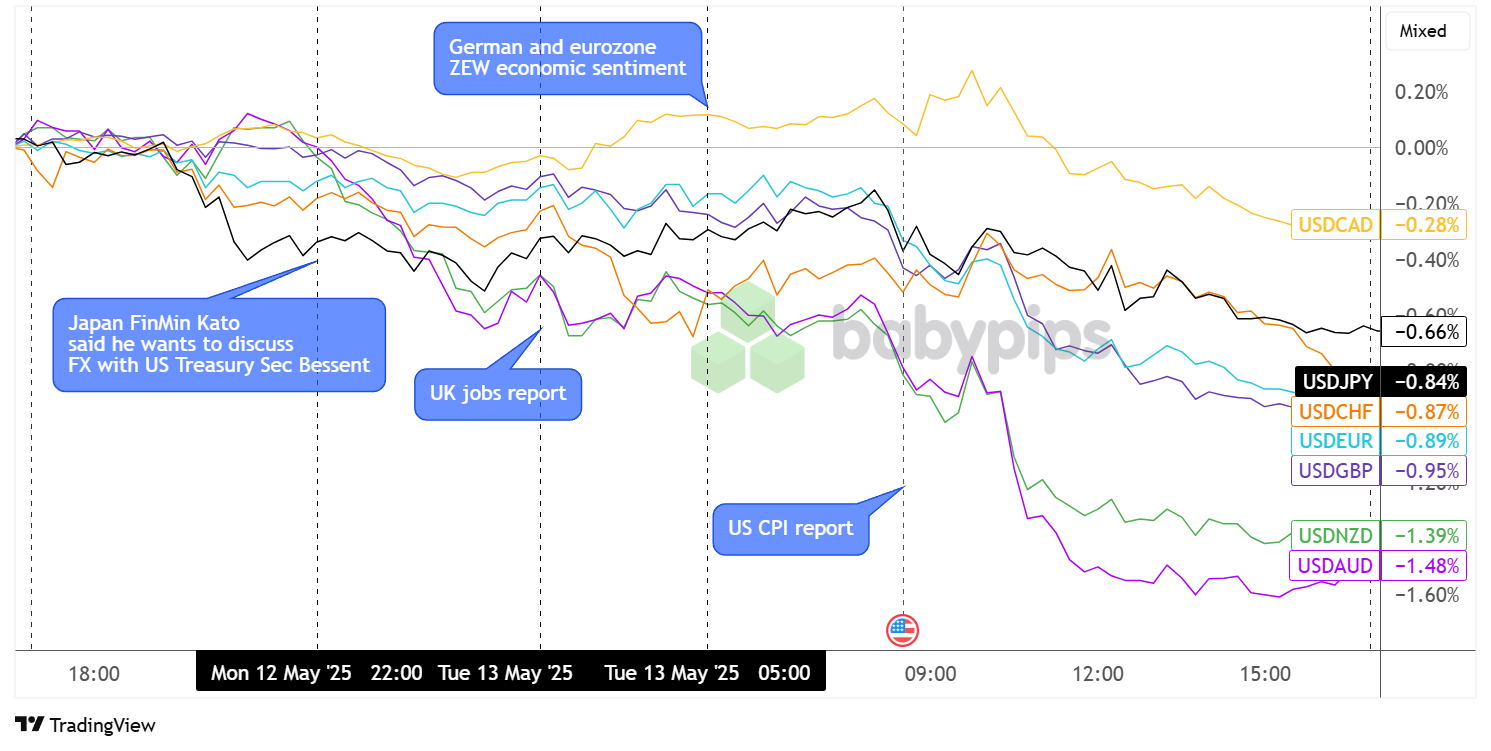

Overlay of USD vs. Major Currencies Chart by TradingView

Currency traders had their fair share of catalysts to deal with throughout the day, starting off with Japanese Finance Minister Kato’s remarks about wanting to discuss FX movements with U.S. Treasury Secretary Bessent during the upcoming G7 meetings, as well as the BOJ meeting minutes which highlighted trade policy uncertainty.

The U.K. jobs release, which turned out net positive with a lower than expected claimant count for April and an upbeat wage growth turnout, failed to generate a sharp reaction from GBP/USD but still allowed sterling to stay supported and close nearly 1% higher versus the Greenback by day’s end.

German and eurozone ZEW economic sentiment readings also beat market estimates and reflected a return in optimism, also putting the shared currency in a good position to take advantage of USD weakness, closing 0.89% higher.

Still, commodity currencies AUD and NZD were the big winners for the day, ending 1.48% and 1.39% higher versus the dollar respectively while markets continued to ride the wave of relief following the U.S.-China tariffs truce. The Loonie, however, was unable to benefit much from oil price rallies, although USD/CAD still closed 0.28% in the red.

Upcoming Potential Catalysts on the Economic Calendar:

- Germany Consumer Prices Index growth rate Final at 6:00 am GMT

- BOE MPC member Breeden’s Speech at 7:15 am GMT

- Fed official Waller’s Speech at 9:15 am GMT

- Canada Building Permits at 12:30 pm GMT

- ECB official Cipollone Speech at 12:40 pm GMT

- Fed official Jefferson’s Speech at 1:10 pm GMT

- U.S. EIA Crude Oil Stocks Change at 2:30 pm GMT

- BOE official Benjamin’s Speech at 2:35 pm GMT

- Fed official Daly’s Speech at 9:40 pm GMT

- New Zealand Food Price Index at 10:45 pm GMT

There’s not much in the way of top-tier data points for today, although it would be worth keeping tabs on central bank commentary to gauge how monetary policy biases may be shifting in reaction to recent global trade developments.

As always, stay nimble and don’t forget to check out our Forex Correlation Calculator when taking any trades!